|

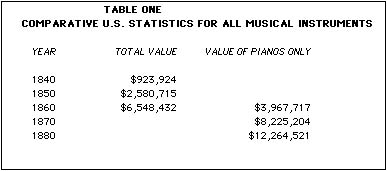

From 1700 to 1750, very few piano sales occurred anywhere. It was just another keyboard novelty. From 1750 to 1800 we see an accelerating pace of interest in the piano. Significant sales were made by the Erards in France, Silberman in Germany, and Zumpe, Clement, Kirkman, and especially Broadwood in England. By 1800 Broadwood was selling 400 pianos per year compared with less than 40 by every other manufacturer. Until the mid 1800's the United States was very dependent upon imports of pianos, in spite of the difficulty in transporting them safe from the effects of humidity. Census reports before 1860 tell nothing of this almost "insignificant" branch of U.S. manufacture (see Table One). | ||

|

In 1850 there were probably less than 50,000 pianos manufactured worldwide. Shops were small and production techniques did not lend well to mass production. England, France, and Austria were the world leaders. The few American and German manufacturers were not yet highly esteemed. Yet, by the Paris exhibition of 1867, the American system was highly honored and the U.S. began its march to take the lead. Only the Germans readily adopted the new system which included economizing the use of expensive skills by substituting machinery for manual work, efficient division of labor, and a world-wide marketing system for supplies and distribution. By 1900 the U.S. had obtained one half of the world market. The second half of the 19th Century saw widespread interest in the piano for the home in America. This led to an interest in the piano for the schools. However, Miller (1988) explains that the upright piano had several disadvantages as a classroom instrument, furthermore, its size and weight prohibited easy transfer from room to room. Thus, many children were probably denied Its benefits. The height of the instrument blocked the teacher's frontal view of the class, forcing the teacher to sit with the back to the class or in an awkward sideways position. Also many believed that the tonal volume and quality were overpowering when accompanying the light head voice typically encouraged in elementary school singing. |

|

||

|

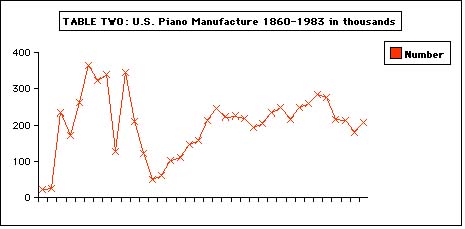

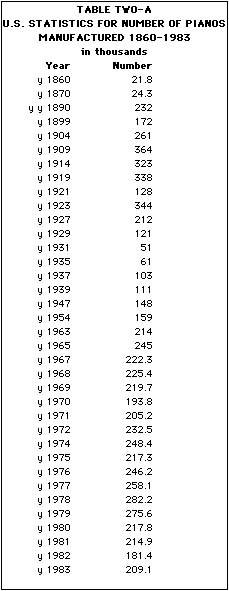

During the peak period from 1890 to 1928, U.S. sales ranged from 172,000 to 364,000 per year with the large uprights getting most of the market. During the last 10 years of this period, smaller upright, 43 inches high, was produced In large numbers by W. Otto Miessner, to meet the demand for a smaller, more portable classroom piano. The introductory price in 1918 was $250. Between 15 and 20,000 units sold between 1918 and 1929. When these Instruments became unexpectedly popular with families living In smaller homes and apartments, the marketing possibilities suddenly became apparent to other manufacturers, Soon they too began to build and sell small pianos, advertising them as "spinets", a term borrowed from the small harpsichords of the 18th Century. | ||

|

In 1928 Miessner traveled and noticed large numbers of pianos in warehouses at rock-bottom prices. He saw the "handwriting on the wall" and was able to liquidate his company before the Great Depression started with the stock market crash of 1929. Many other American piano manufacturers were forced into bankruptcy between 1929 and 1931 (Miller, 1988). From 1900 on the piano, now well established as a versatile

concert or home instrument, followed trends in the times (see

Table 3 and 4). The maintenance of great interest in pianos from

1900 to the depression was aided by enthusiasm for player pianos,

especially in the early 1920's when 500,000 were made every two

years. After the Great Depression of the 1930' s, recovery was

slow due to the development of alternatives to home entertainment

such as the gramophone, radio, record player, television, and

on to the tape deck, compact disk, and even the electronic musical

instruments, satellite television, and computers. The slow, steady

growth of U.S. piano sales since the 1950's far from

reflects population growth. In the 1970's, Japan (and particularly

Yamaha with an annual output of over 200,000 units) took over

as the top producing nation. Throughout the 1970s and 1980s,

Japan has continued to produce about 300 to 400,000 per year.

The U.S. approached this only during the period 1909 to 1919.

|

|

||

|

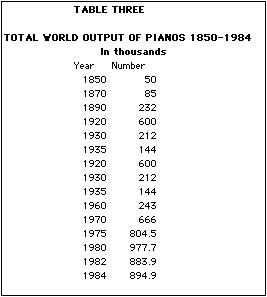

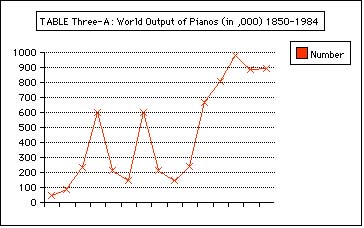

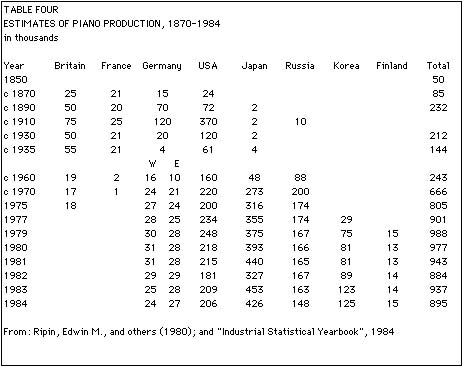

Table Three illustrates that the world output of pianos followed the U.S. trend, a tremendous drop in 1930, followed by a long, slow recovery period. In the 1980s there is another tendency for the numbers to drop, but only after a tremendous peak in 1979 of 988,332 pianos worldwide (Industrial Statistics...1984). Table Four shows how piano production leadership has shifted from one country to another through the years. Austria began as an important producer in the early developmental period of the piano, but now produces less than 800 pianos per year. France and Britain likewise did not maintain their 19th Century enthusiasm for piano manufacture into the 20th Century. Japan started late (1890s), and slow (only 2 to 4,000 per year), but took the lead In 1970 and keeps it by a wide margin with well over 400,000 produced annually. In recent years Korea has begun to play an important role in the world piano market, being well over the 100,000 mark since 1983. Finland first went over 10,000 per year in 1978. |

||

|

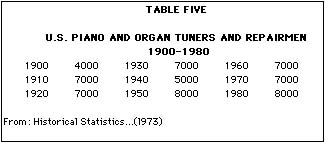

One can imagine that given a life expectancy of 50 and up to 100 years, and the perhaps 50 million pianos sold during the past 100 years, how many millions there must now be stored, or in use. There are nearly one million produced each year now, worldwide. Yet Table 5 indicates that the numbers of tuners and technicians has not proportionately Increased. Is it becoming harder each year to find a piano tuner, or are the instruments being grossly neglected? Economically, the piano industry Is still as important today as it was in 1860 when it was said that "first in Importance stands the piano-forte ' (Manufactures ... 1860). The wholesale value of pianos produced in 1967 In the U.S. was $91.2 million. Between 1972 and 1982 the value ranged from $107.4 to 230.8 million (Bureau of the Census, 1982). The 1987 wholesale value was $130.8 million compared to organs, 184.2 million (Corea, 1988). The retail value of pianos sold each year during the late 1980s probably approaches $625 million for those manufactured In the U.S., and +2.29 billion worldwide. Twenty-five percent of the U.S. made pianos that are exported go to Japan and 15% to the United Kingdom. The United States received In 1987, 66% of its imports from Japan and 14% from Korea. The 1997 Census reports only ten piano manufacturers in the U.S. with eight manufacuturers of "vertical, upright or console pianos", and four producing grand pianos. The total wholesale value of pianos in 1997 was $185,738,000, a 203% increase since 1967, with 1,455 employees. |

|

||

|

"Pianos are seen as an investment, whose intrinsic value outlasts economic downturns... According to a survey funded by the American Music Conference, at least one amateur musician was included in the 51% of the households responding...more than 50 million 'amateur musicians', compared with 31.5 million In 1970... The combination of rising income and greater leisure time has played an important role in the growth of the music industry (Standard & Poors, 1981). | ||

|